- The Quench Report

- Posts

- New To World For The Win - Quench Report Issue #35

New To World For The Win - Quench Report Issue #35

Plus: Nowadays Launches Extra Light, Hot Jobs and More

Matt Rice

April 27, 2026

Taking a break from Brown-Forman this week to dig into something else: why the recent M&A wave (Beatbox, Monaco, The Long Drink, and others before them) will continue and what it tells us about who wins next.

What’s on tap for today:

🥇 Deep Dive - New To World For The Win

🆕 Nowadays launches Extra Light

🔥 Hot Jobs Worth Applying To

🥇 NEW TO WORLD FOR THE WIN

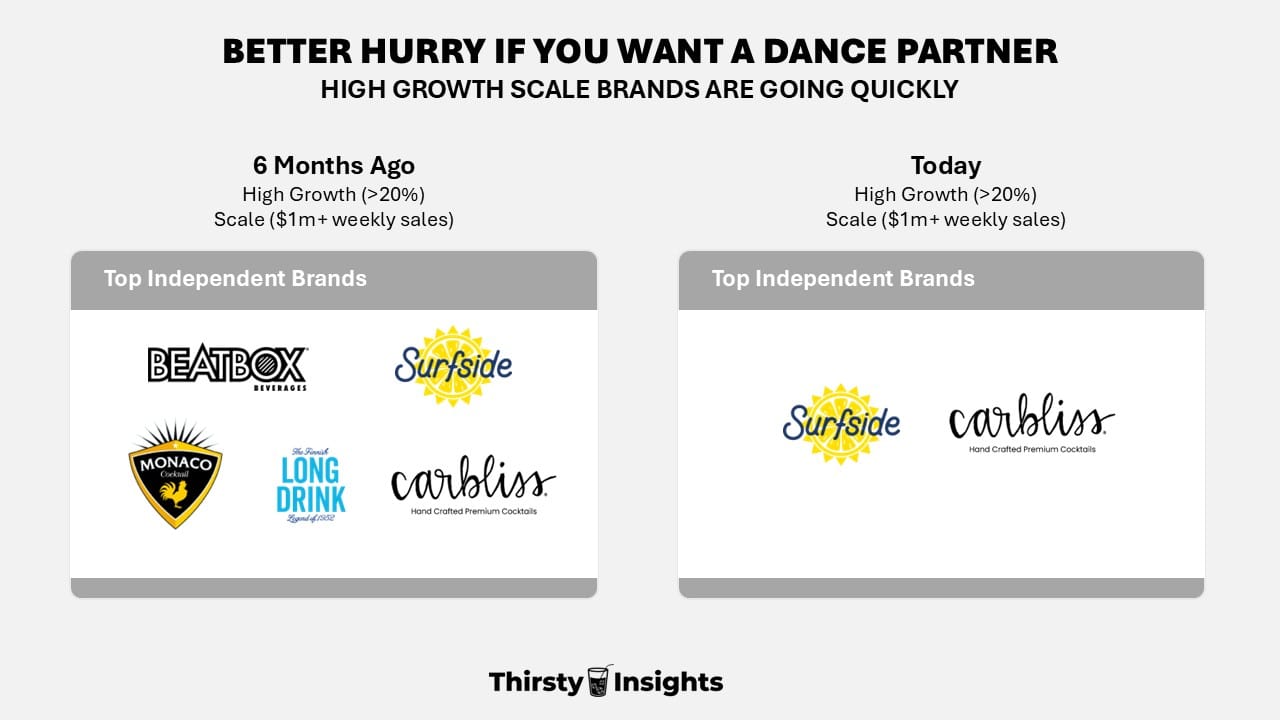

Last week, on the heels of The Long Drink's acquisition, we put a graphic on LinkedIn showing how quickly the fastest-growing independent bev alc brands have been getting picked off. See below for a reminder 👇️

The size and growth bar in that analysis was admittedly arbitrary, and there are plenty of smaller high-growth brands not on the list. But the picture is clear: the fastest-growing independent brands are getting acquired fast, there are fewer of them now than a few months ago, and there's still no shortage of large suppliers who need them.

That raises two questions worth digging into:

Line extension or new-to-world brand - which one actually captures an emerging category? The pattern is clearer than you'd expect.

Why would large suppliers, sitting on powerful, consumer-preferred portfolios, pay up to acquire much smaller new entrants in categories they are already in?

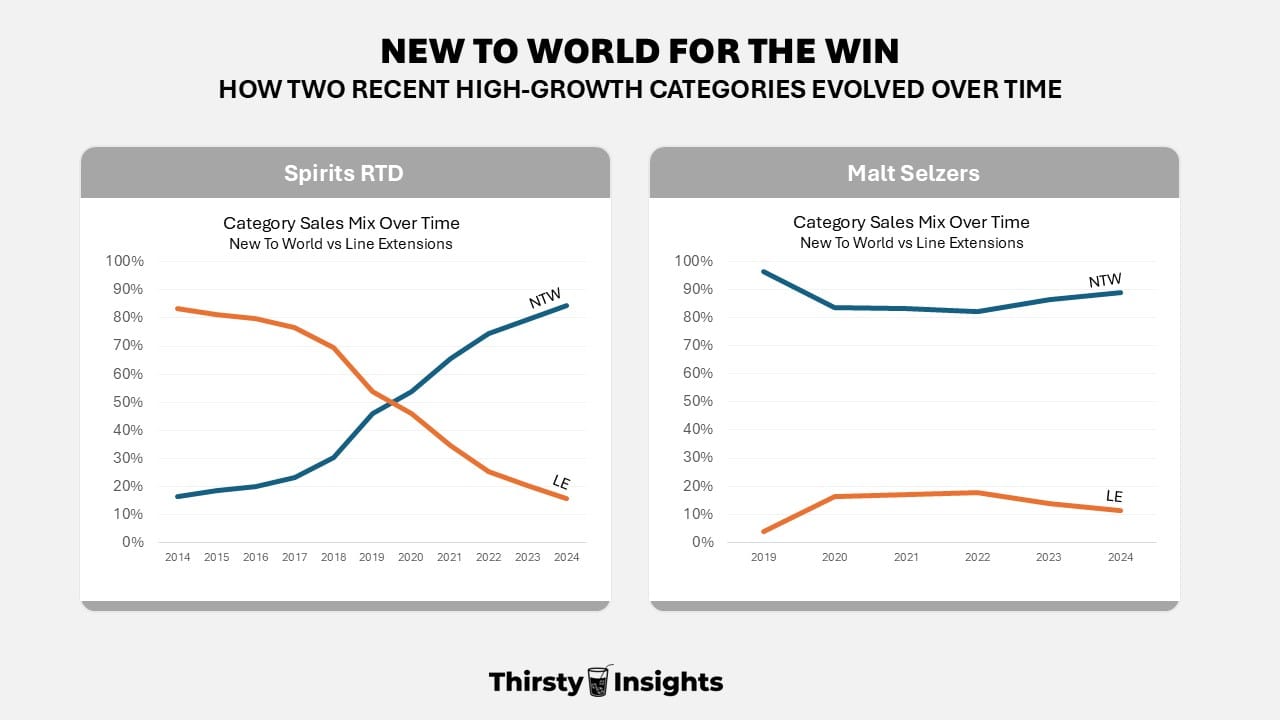

The first question has an easy answer: in nearly every case researched, new-to-world (NTW) brands end up winning emerging categories. Want proof? Look at how two recent high-growth categories evolved 👇️

A few notes about the data and the pattern:

Spirits RTD - The incumbents weren't asleep. Most major spirits brands had RTDs in the late 2010s, Malibu Rum cans as an example, and the line extensions were winning. In 2017, they were outselling NTW brands like Cutwater and the just-launched Long Drink by a wide margin. That dynamic held for years. Then in late 2019, NTW brands pulled ahead for the first time. The lead has only grown. Today, the category belongs to them.

Malt Seltzers - Different start, same finish. NTW offerings (White Claw, Truly) led the early category. By 2019-2020, the major beer brands flooded in with line extensions, Bud Light Seltzer chief among them, and there was real industry chatter about whether the massive incumbent beer brands would knock the originals off their perch. They didn't. The NTW brands fought back, regained share, and now control nearly 90% of the mature category.

❓️ WHY DO THESE NTW BRANDS END UP WINNING?

Consumers often prefer brands "born" in a category - When a brand is purpose-built for a specific occasion or category, consumers read it as more authentic… designed exactly for this, not stretched into it. A line extension carries the baggage of the parent brand and signals "borrowed credibility." An NTW brand starts with a clean slate that consumers interpret as conviction.

NTW Brands Burn The Boats - A line extension doesn't have to “work” to survive. It can underperform for years on the parent brand's shelf space, distributor commitments, and trade marketing budgets, long after consumers have voted with their wallets. NTW brands get exactly one shot: nail the proposition or die. That pressure forces a level of product, packaging, and positioning rigor that line extensions almost never match.

Line Extensions Inherit “Legacy” - Line extensions get the parent brand's existing flavor houses, creative agency, sales playbook, distributor relationships, and route-to-market strategy, all optimized for the main product’s category, not necessarily the new one. That looks like efficiency, but in a category with different consumer dynamics, channel economics, or buying occasions, those defaults can be an active disadvantage. NTW brands pick partners for the job in front of them.

THE FINAL WORD

Line extensions off powerful brands can absolutely work, and a few have moved real units.

But if history holds, the winners of the next hot category will be NTW brands born into them, which is exactly why strategics keep paying premiums to acquire the ones already pulling ahead.

🆕 NOWADAYS LAUNCHES EXTRA LIGHT

Late last week came word that leading Cannabis beverage maker Nowadays is launching a “light” version that meets the 0.3% THC content threshold rules that are set to be active in November.

In a statement, the California-based group said it was “safeguarding itself” with the new Nowadays Extra Lite, which will contain 0.4mg of THC and 5mg of CBD. Check it out below 👇️

Two of the SKUs in the Nowadays Extra Light range. Credit: Nowadays

This is the first proactive launch we can think of from a brand reformulating toward a regulatory threshold that didn't previously constrain them. Expect more of this as November approaches, distributors and retailers are already turning risk-averse, and that pressure will only intensify as the deadline closes in.

We know only a portion of our readers operate in THC beverages. But the strategic decisions playing out in this category right now are genuinely fascinating, and a few of them will end up as business school case studies. Even if you're not in the space, it's worth tracking how these brands are navigating the regulatory shift, the playbook will be relevant the next time your category faces one.

THIS WEEK’S HOT JOBS IN BEVERAGES

These roles came to us via ThirstyTalent.ai. Want your open role featured? Email: [email protected] 👇️

Manager, Consumer Insights - Mark Anthony - Chicago, IL

CMO Spirits - Confidential - Los Angeles, CA

Market Sales Manager - Milestone - San Antonio, TX

Sr. Director Innovation - La Colombe - NY, NY

Finance Director - Owl’s Brew - Remote

Sales Consultants (multiple) - Winebow - California

THANKS FOR READING

The Quench Report is a free weekly newsletter from Thirsty Insights, a beverage alcohol consulting company that serves top clients in data, strategy, insights, and analytics.

Any questions, please email us at [email protected]